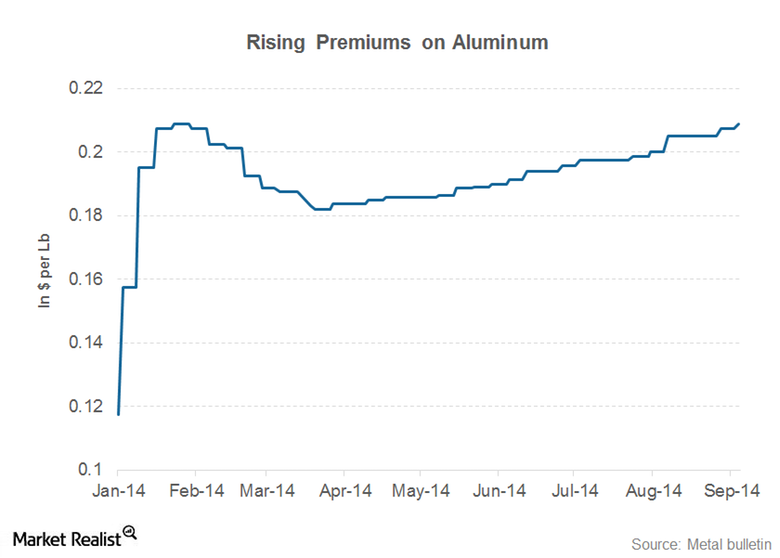

Another month passed in the New Year and there is still a good amount of hullabaloo in the market about the aluminium premiums and price of the metal. LME Aluminum benchmark prices rose to $2,114 in 2014 Aug after hitting a four-year low and presently it is hovering between $1,700 and $ 1,800. However, premium is another component in aluminum’s price which is equally crucial for aluminium producers, investors and consumers. As the LME glossary says premium is a one-off payment, made at the outset, to purchase an option which in this case is the physical metal. So it is the price that is paid to get physical delivery of aluminium. It includes the cost of freight and handling to ship aluminum from LME warehouses to other locations.

The major drivers of premium are demand, supply, LME cash price, freight, warehouse rent, cancelled warrants and trading costs. However, the main factor that influences premiums is the broad gap between demand and supply in the market. When markets are tight and the metal is not available to buyers, premium tends to increase and it tends to decrease when markets are oversupplied with metal and there are more sellers than buyers.

Premiums are quoted over and above the LME cash price and vary according to the locations in which the metal is delivered. Premiums are mutually related to the LME cash price as each has an influence on the other. Aluminium premium is normally quoted for three benchmark locations, Europe, Midwest US and Japan.

However, the normal equation between aluminium premium and demand supply seems to be disrupted in last few years. Aluminium inventories in LME warehouses have gone up excessively in last seven eight years due to industrial slowdown and demand plunge associated with the global financial crisis after 2008-2009. When there is excess supply of the metal premiums should come down as a norm. But the aluminium premiums started soaring throughout the years and hit record highs.

Market experts have pointed towards two main reasons influencing this continuous rise in premiums: Easy financing for aluminium inventory (carry trade) and Cancelled warrant queues.

Stock financing or carry trade has been influencing premiums and warehouse backlogs for pretty long. Under this strategy, an investor borrows money at a low interest rate in order to invest in the metal that is likely to provide a higher return in future. As cheap financing is available for buying metals and due to wide market contango, investors prefer to buy metal which will be delivered at a future date. Warehouses offer low rents for metal storage and high incentive due to which investors pay a premium for the metal to get it delivered at some point in the future than paying the actual expected price of the commodity at that future point.

This strategy created business opportunities for some banks and traders who even acquired warehouse companies to stock aluminium. Owning warehouses allowed them to earn revenue from rental charges and cut down the storage cost for the metal units they owned under cash and carry deals. As a result, the metal got locked in warehouse and was not available for physical consumption. Financial demand for metal drove up incentive and tightened the market for physical metal which in turn raised premiums. Aluminium buyers even accused that the long queue for the physical delivery of the metal actually raised the premiums. Market experts have considered this financial arbitrage to be highly responsible for the sky high premium levels of the last few years.

As a result, in December 2014, US aluminium premiums were ruling at $500 per tonne. In Europe, the level was a bit below $500 and in Japan premiums were at about $420 per tonne. During January 2015 it was hovering above $500 per ton. In case of Asia the benchmark premium for the first three months of 2015 has been around $425 per tonne over LME cash price. It was a rise of $5 per tonne from the last quarter of 2014.

However, with the beginning of 2015, this financial arbitrage has begun to ease slowly; hence, the downturn in premiums recently. The arbitrage has eased with a narrowing in the contango (futures price minus spot price). Cash-to-3-month simple arbitrage contango narrowed to $13.52/tonne from a $14.59/tonne in January. As a norm, longer the narrow contango persists the more inventory will flow to the market. During a contango situation, if the difference between the spot price and the futures price is greater than the cost of storing and delivering the commodity, then there is the potential for arbitrage. But presently the cost of storage is more than the difference between the spot price and the futures price. It is now becoming less profitable to hold material in warehouse as the premium level does not justify paying the storage cost.

So, the market seemed to take a turn during the month of February especially in the European market. The US Midwest aluminium premium was also on a downward curve throughout February, the reason for which has been cited as rising imports putting pressure on the demand supply balance in the domestic market. According to AMM’s assessment of spot P1020 premiums, it eased to a range of $ 484-490 per tonne plunging from a record high of $ 528-533 in mid-January. In view of market participants the demand and consumption is strong in the US coupled with a very attractive premium, so material flows there. They expect the premiums to settle at $ 462 – 473 in near future.

The spot aluminum premium for the Japanese buyers has currently come down to $370 per tonne, plunging from a high of $425 per tonne. One factor to be considered here is that premiums tend to equalize globally and a drop in one region encourages a drop in another.

Metal Bulletin’s duty-paid aluminium premium for Europe is presently hovering within a range of $375-420 per tonne which is a big plunge when compared to last quarter. According to market analysts, falling demand and an increase in the availability of aluminum scrap and primary metal have pushed premiums lower in Europe. Europe also has the largest stock of metal outside LME registered warehouses. There is also more than enough of supply from Russia, China, India and Middle East. With such high availability of metal in the spot market, cancelled warrants are not working because the costs for holding metal in warehouses are quite high. With people unwilling to store metal for physical delivery at a later stage, the metal is sure to flow to the market. A large amount of metal had been loaded in LME warehouses but at the same times there was equal amount of load outs. (LME stockpile has now hit 4.08 million which is the lowest since 2009)

One reason for the metal to flow to the market could be the new LME rules which require warehouses to ship out more aluminum than they take in after a period exceeding 50 days. This rule which is supposed to get implemented from February is expected to force excess inventories out of warehouses. LME also set a firm October 26 date for the launch of aluminium premium contracts. The aluminium premium contract will allow people to hedge additional surcharges for buying aluminium for immediate delivery. LME expects this contract to appeal to investors who are locking in future premiums hoping for profits.

Considering the deficit in aluminium, if the market turns towards backwardation where spot prices are higher than futures, then outside LME warehouse owners might release stocks in the market causing a drop in premiums. With Higher global production, unwinding of warehouse storage deals, constant flow of inventories to the market and rising exports of aluminium products from China, the artificial shortage of aluminum should come down and it should check the rising premiums. As a whole, we can expect a balanced and bearish situation for aluminium premiums in 2015-2016.

Reference:

http://www.metalbulletin.com/

http://www.crugroup.com/

http://www.reuters.com/

(Disclaimer: The information presented in the article is author’s observation based on available market data and information and neither intended nor implied to be a substitute for professional advice.)